| UK House Sellers In Denial About The Property Crisis - Energy Too? | The Oil Drum: Europe | The First Wave Energy Farm of the World...It's About Time... |

Some Lessons from Bailout Month

Posted by Jerome a Paris on October 1, 2008 - 10:20am in The Oil Drum: Europe

Despite the first rejection of the Paulson Plan, the effort is ongoing in Washington to push through a plan that is likely to be substantially similar to the first one (as far as I can tell, the only changes will be tax cuts and the inclusion of the renewable energy bill items). Given the overwhelming pressure to "do something", and despite warnings that we are being rushed for no reason into a terrible plan, it is rather unlikely that the final version of the plan is going to be very satisfactory. In any case, the following will hold true irrespective of the outcome of the Paulson Plan.

(Note: This was written for the European Tribune this week-end, ie before the rejection of the plan by Congress, and before the most recent bank bailouts, but its conclusions stand)

- the consequences of the financial crisis are so dire that the lesson here should not be that a bailout is necessary (it is, at this point) - but to acknowledge that the financial sector has the power to hold the rest of the economy to ransom during both good times and bad times and thus that it need to be emasculated so that we never get again to the stage where a bailout is necessary. The lesson is that the financial world cannot behave responsibly, if left to its own devices and thus should not be left to its own devices;

- another is that the main argument to give financial markets a free hand — that they have created so much growth and prosperity — needs to be called for what it is: a lie. Not only the so-called prosperity of the past year was highly unequally shared (see the next point), but it was not even real, as the income and profits of the good years are now dwarfed by the losses of today. Arguments about growth need to be dismissed by a reference to the "full cycle," i.e. the prosperity of the recent past can only be accepted as real if it wasn't a capture of the prosperity of today and the near future. If the forthcoming growth and GDP numbers are dismal, this should be seen as a direct proof that the growth of the past was nothing but, and that the policy prescriptions focused on financial profit are abject failures;

- as the bailout calls for yet another transfer from poor to rich, it is worth noting that even in the good years, the vast majority of the population saw very little of the then much touted prosperity: incomes were stagnant or declining, while benefits declined, and healthcare and energy costs skyrocketed. Thus, current policies seem focused, at all times, on maximizing the income of the few rather than that of the general population;

- the next conclusion is that our political systems are completely geared towards fulfilling that last goal: politicians of all stripes are supporting the bailout despite massive protests by their constituents, just like they supported financial deregulation, labor market "reform," "free" trade, the tax race to the bottom and other similar policy prescriptions in the past. Politicians are supported in that by a media system that brings to the fore pundits that are fully aligned with these prescriptions, and creates an incestuous class of insiders who, as it were, tend to personally benefit directly from the overall winner-takes-all policies put in place;

- the quasi-unanimous support of the Serious People for the bailout, or at least their inability to point out that the current crisis was the inevitable conclusion of the policy framework pushed by the neolib cabal shows how successful they have been at killing alternative ideas as fringe or absurd or dangerous, and suggests that there still is an ideological vacuum; alternative ideas are not "there" enough to be taken seriously despite the ongoing reality, and I'm not sure they will until the current elites are completely pushed out;

- given that staying in power and doing whatever it takes to achieve that goal is their main competence, I fear that we're going to be pushed into ever more dangerous brinkmanship, as the Republicans have amply demonstrated in recent days. They will not leave without a fight, even if reality is overwhelmingly against them, and I expect obfuscation, distraction and worse to be used to deny or avoid that reality. Quite frankly, the alternative now, just like in the 30s, is either a full break from the past (a new "New Deal") or a move towards fascism and war — the latter being our current elites' only chance of holding onto power.

In other words: nothing short of a revolution will do. Can it still be a peaceful, democratic one?

Personnel

Editors

Contributors

Peak Oil Primers

Archives

- November 2010 (3)

- October 2010 (6)

- September 2010 (4)

- August 2010 (7)

- July 2010 (6)

- June 2010 (7)

- May 2010 (2)

- April 2010 (8)

- March 2010 (4)

- February 2010 (6)

- January 2010 (3)

- December 2009 (5)

- November 2009 (8)

- October 2009 (12)

- September 2009 (6)

- August 2009 (5)

- July 2009 (11)

- June 2009 (8)

- May 2009 (16)

- April 2009 (10)

- March 2009 (7)

- February 2009 (10)

- January 2009 (15)

- December 2008 (9)

- November 2008 (9)

- October 2008 (9)

- September 2008 (13)

- August 2008 (10)

- July 2008 (14)

- June 2008 (23)

- May 2008 (16)

- April 2008 (12)

- March 2008 (16)

- February 2008 (9)

- January 2008 (13)

- December 2007 (13)

- November 2007 (16)

- October 2007 (22)

- September 2007 (8)

- August 2007 (9)

- July 2007 (16)

- June 2007 (8)

- May 2007 (7)

- April 2007 (7)

- March 2007 (10)

- February 2007 (10)

- January 2007 (12)

- December 2006 (9)

- November 2006 (15)

- October 2006 (4)

- September 2006 (5)

- August 2006 (5)

- July 2006 (9)

- June 2006 (5)

- May 2006 (10)

- April 2006 (9)

- March 2006 (13)

Vital Trivia

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

The FT has the opposite conclusion, in their main editorial:

Yeah, right - the only policy decision of note after 1929 was Smoot-Hawley. Not the regulation of banking and the New Deal. Interesting vision of history...

Yes, let's focus on the short term: it's true that Wall street can take down Main St with it. That would seem like an additional argument for clipping Wall St's wings, not a mitigating factor - but hey, what do I know?

Deregulation = bad regulation = government sucks

The chutzpah is quite amazing, really. They pretty much got all the deregulation they wanted, and all the downside protection the financial sector wanted, and now the government is to be blamed because it obyed the financial sector's every wish?

Isn't the point we're at today pretty much that failure is NOT BEING PUNISHED????

Matchless indeed:

The only silver lining is that, for the first time in a long time, they sound a tad defensive to me...If they feel the need to argue they are not a "fundamentalist religion", we're finaly making progress. yey!

Here is a video from Karl Denninger that is interesting.

**FLASH** The REAL REASON For The Bailout

http://uk.youtube.com/watch?v=GqIFoBXGizc

LOL -- No Banker Left Behind

COL -- 700B of Shanghai junk paper

Karl Denninger is the man. Unfortunately, the Argentinization of America is proceeding right on schedule. Realistically, if you want to predict the actions of the USA federal government on any issue you simply need to look at the effect on the roughly 1200 global billionaires. This is a lot of fun for those guys so they need to push it through regardless of public opposition or the effect on the economy. This is just the beginning.

Also, Paulson is the lead guy, but a lot of "squeaky clean good guys" are out there screaming loudly for this bill-Barack Obama and Warren Buffett are just two of them.

Sold to you.

It's often as much about what is NOT said or written...

Thanks to Mish...

Rep. Brad Sherman On Bailing Out Foreign Investors

Here is a video clip explaining the foriegn bailout of the banksters with the MSNBC clip emedded near the beginning.

http://www.youtube.com/watch?v=Q4AvbYUu1Mg

It is outrageous that the US taxpayer will bail out Chinese, Japanese, British, Aistrailian, etc., toxic debt.

GROCK, just went there and got this: This video has been removed by the user.

It didn't say anything about the bailout having to include foreign interests in order to protect the derivative market did it?

Hello Ignatz, that is very curious! Yes there is a provision that would allow foreign banks that have an American presence to dump toxic financial instruments onto the "bailout" plan. I am concerned that we are witnessing the clampdown of free-speech.

Found the link directly to his website:

http://market-ticker.denninger.net/archives/596-The-TRUTH-About-The-Bail...

Did the Big-Boyz come down on YouTube? Was it swamping their servers? If so that would be good but if it was the Plutocrats taking him off then the fix is in.

THE FIX IS IN, THE PATRICIAN SENATE CARES MORE ABOUT THE BANKSTERS AND FOREIGN BANKS THAN THE WORKERS AND MIDDLE CLASS.

NO TAXATION WITHOUT REPRESENTATIUON:THE SENATE HAS LOST ITS RESPECT FROM THE AMERICAN PEOPLE, NOW THE HOUSE WILL BE TESTED AGAIN.

Hello Ignatz, that is very curious! Yes there is a provision that would allow foreign banks that have an American presence to dump toxic financial instruments onto the "bailout" plan. I am concerned that we are witnessing the clampdown of free-speech.

Found the link directly to his website:

http://market-ticker.denninger.net/archives/596-The-TRUTH-About-The-Bail...

Did the Big-Boyz come down on YouTube? Was it swamping their servers? If so that would be good but if it was the Plutocrats taking him off then the fix is in.

It's not curious, it's a choice.

If they do not allow foreign banks to liquidate the toxic debt they then no foreigner will touch US assets or the $. All the dollars held abroad will be repatriated and the dollar is toast.

So either they hyper inflate or the dollar is toast, and if they do inflate then the $ is toast anyway.

That is the true dilema and there is now no way out. All they can hope for is to stall for time.

When the crissis hits in full global trade will collapse.

Since the US is importing so much oil there will then be an immediate energy crisis for the US. Followed by war or should I say more war.

Try this

http://supportedthebailout.org/

Thanks musashi, All the rape you can stand in less than one minute?:)

youtube does other things to hide inconvenient videos - like the complete SNL Palin/Clinton skit video address, which youtube kept replacing with a shorter FOX News report on the skit instead.

I have lost respect for YouTube then.

My son sent me an URL for the SNL Palin spoof: http://www.nbc.com/Saturday_Night_Live/video/clips/couric-palin-open/704...

I just checked it, it still is there.

My son sent me an URL for the SNL Palin spoof: http://www.nbc.com/Saturday_Night_Live/video/clips/couric-palin-open/704...

I just checked it, it still is there.

Denninger is wrong.

It has everything to do with Main Street, with sending your kid to college, with buying a house, a car, the WHOLE AMERICAN PIE.

If Paulson isn't allowed to appease our creditors it is the end of "The American Way of Life".

Don't listen to Denninger or Mish or any of the others because this Bailout is about our ability to retain GLOBAL reserve currency status and therefore dominance, and therefore keep a quarter of what the world has to offer flowing in our direction.

Which they will fail to do but they have to try.

After this failure they have to try to keep the bootie flowing , as outlined in the Economic Hitmans Bible, at the point of a gun.

Which they will fail at also but…

What effect will this have on Peak Oil? HHHMMMMMMMMmmm?

I know, too cynical for you all. Lets armchair QB the political machinations instead. BS!

Revolution

Denninger is sometimes a good read. But this clip is absurd.

The argument that the Bail Out should be opposed because the money will fly overseas is pure demagogery - condescending, trite.

Note he gives absolutely no reason why the US / Bush / Paulson / etc. would do such a thing. If he wants to paint them as evil madmen (which they may very well be) he has to add a little something to his argument.

Adding something would mean describing the situation better, e.g. to be very mild, that global finance is so complex that the appellation ‘foreign’ is meaningless; or, more forcibly, that the bad paper is spread about and some very powerful entities hold huge amounts of it.

In the US, nay sayers are sometimes even clumsier and dopier than the PTB. Shame on them.

Hmmm...so Paulson's refusal and Bush's veto of the plan if the foreign bank provision was removed is not salient. I believe your belief that they would not bail them out is contradicted by their actions. Observe them in action. First they tried to blast the bill through using scare tactics. Then Paulsen said he would brook no changes. Now a part of the bill has been exposed to bail foreign banks. What else do we not know of at this time? Have they been truthful?

I've got a beautiful bridge in Brooklyn I need to sell you ASAP!

Perhaps, (and I admit this the viewpoint of a non-American citizen), if there is to be a bailout plan, why shouldn't it also bailout foreign investors who are suffering the fall-out of the mess created by US financial madness?

I'm not saying I like the bailout. In fact I think that it is indeed just another way to get taxpayers to pay for the mess created by rich and wealthy. The rich and wealthy get bailed out, and there aren't even any provisions in place to make sure this doesn't happen again. It is bascically saying, go ahead, take silly risks, the tax payer will bail you out if things go wrong.

But then again, if there is to be a bailout, why should foreign investors, who are just a much a victim of this US created madness not get bailed out as well?

The problem was not created by the working class in the US, and that is who would have to shoulder the bail out. If foreign investors took a risk of participating in this mess, they also took the risk of enjoying the rewards if it was successful.

The problem here is painting with Broad strokes, The problem started in the US, but only by a small number of folks. the ones who are responsible for this mess are not being held accountable. The ones who will end up paying for it had little to do with it. The idea of further passing on the burden of the global consequences to the working guys and gals who will have to pay for the irresponsibility of the likes of Paulson and Co. is distressing. We should make Wall Street pay for it, nationalize their assets, their McMansions on Long Island, etc, and if that still does not cove the costs, we should demand a hefty price in pounds of flesh from these criminals.

How many of the working class voted for George Bush though?

In a democracy, the voters are responsible for which government officials they elect. Surely that is the idea behind the system.

I'm with you Bob. If people are too stupid to understand the consequences of their votes, they deserve what they get...I'm just sorry me and mine get those consequences as well.

1. If there is one group of people who are "too stupid", then surely there must be another group of people who are "too smart".

2. If there is one group of people who "deserve" bad consequences, then surely there must be another group of people who do not deserve the same.

3. It does not take a whole lot of guess work to understand which groups are the ones the speaker instinctively places himself in without saying so out loud.

4. Also the agreeable listener will automatically place him or herself in certain ones of these groups and "laugh" at the other groups for being too stupid, ha ha, and being "deserving" while subliminally appreciating that the listener is both too smart and wholly "undeserving" of that or any other bad fate that falls upon the "others". (Hurray for our team, tough luck for them other people.)

So with that in mind, let's make a hypothetical list of people who were "too stupid and "deserved" what they had coming to them:

... mentally challenged students who are ordered by their teacher to march off the edge of a cliff and do so just like lemmings ...

... the brainwashed children at Jones Town who drank the "Kool aid" when instructed to do so by their parents ...

... the victims of the Nazi Holocaust who willing marched onto the death trains under the belief they were going to a "relocation" camp ...

... each of us who has ever eaten a hamburger at McD's ...

... each of us who has ever gotten addicted to nicotine ...

... each of us who has ever gotten addicted to caffeine ...

... each of us who has ever vegged out in front of the TV (boob tube) ...

... each of us who has ever voted for Party A instead of B even though there is no real difference and we're going to get what we "deserve" irrespective of which way we vote because many of the games played in this world are tails-you-lose and heads-they-win games ...

So yes, those "others" were too stupid and "deserved" the bad consequences that befell them.

I'm laughing.

You should be doing the same.

Unless of course, you are one of those "too stupid" people or one of those people "deserving" of a bad fate.

Thank you. Dead on. I'm with stupid.

Books on stupid:

Just How Stupid Are We? Facing the Truth About the American Voter

http://www.amazon.com/s/ref=nb_ss_gw_0_9?url=search-alias%3Daps&field-ke...

Dark Ages America: The Final Phase of Empire

http://www.amazon.com/Dark-Ages-America-Final-Empire/dp/0393329771/ref=p...

You've totally missed the point. Voters are not mentally challenged nor in death camps, they are responsible adults. That is the argument for why there should be democracy and not royal prerogative for example. If people give up their hard earned right to select good leaders, and allow a de facto dictatorship, then complain about the poor quality of the leadership - is that not willful stupidity?

"... victims of the Nazis...."

Godwins Rule.

My working premise is that they were brain washed into voting for the "W" (movie coming soon).

They didn't have a fighting chance because them that know what we fear used that avenue into the subconscious to control how the American working class behaved. It's not a matter of "responsible adults" getting what they "deserve" because they act stupid. It's a matter of people who know how to control the masses through thought manipulation taking advantage of their advanced knowledge in evil ways, just like an instructor who guides special children over the cliff's edge. Why do we always blame the victims? Don't the evil doers deserve some of our attention? Do they "deserve" to get away with their crimes? No.

I totally agree. The bailout is not holding the right people accountable.

All I was saying is that IF the bailout goes through. It seems only reasonable to bailout the foreign investors too.

But yeah, I do agree. Those who created the mess should be the one paying for it. Foreign or US/domestic alike.

They snuck in a provision for the banks to have ZERO reserves. Infinite lending with nothing to back it. This will guarantee that the banks are trusted... Right...

They snuck in a provision for the banks to have ZERO reserves. Infinite lending with nothing to back it. This will guarantee that the banks are trusted... Right...

There is one reason I can think of right of the hat: The owners of the countries mentioned might be really pissed off at having been had with all those beautiful investment vehicles the smart boys & gals at Wall street invented.

They might want some of their money back, and being the rich boys from over there, they could have the clout to get some of it.

The big bullies fighting over the loot of the school, leaving all the kids bruised and battered in exchange for all their money and i-pods&phones.

Pathetic. Pathologic.

Paulson is the messenger.

Acting in his capacity of member of the board of directors of the IMF, not as treasury secretary, this is why he can afford to be so arrogant.

He is Guido with the baseball bat, the senators are the drunk daddy that lost his paycheck at the poker table and likes to keep his knee caps, and the tax payers are the babies crying in their crib for a tit to suck on.

Daddy has no balls and the kids don't want to grow up.

Noizette

I'm guessing all this is to protect the derivatives market and as that is global then foreign banks must be included, but in that case I would think Denninger has a point that the cost shouldn't be carried by the US taxpayer alone if they are carried at all.

"Adding something would mean describing the situation better, e.g. to be very mild, that global finance is so complex that the appellation ‘foreign’ is meaningless."

But "US Taxpayer" is not meaningless.

This bill is a monstrosity.

Whenever you hear some grifter use the words "finance" and "complex" in the same sentence, hold onto your wallet and check that your watch is still on your wrist.

Too late ... they're both gone.

Even if passed, give it a week or two and you will be proven wrong.

The hit main street will take in the short term is the exact same with or without the bill, in the longer term it is much worse with the bill.

Passing the bill may buy you a week of dead cat bounces. If that.

I agree. The markets should be hard down this month, in the first of several cascades over the next couple of years. The bill is an opportunistic power grab that will do nothing at all to prevent the great deleveraging that is underway, but will leave a legacy of unaccountable power, ripe for abuse.

I do expect a significant rally into the end of the year though, probably following a temporary bottom (a spike low?) near the end of October. My guess is that the decline would resume, with the beginnings of the next cascade starting in the New Year. 2009 will be the year when Wall Street takes Main Street down with it.

No. Nada. Nyet. My dear Souperman2, it may be the end of "your" American way of life, but not the end of the many many, millions who live a responsible life. American Pie? Well I guess it's "Bye Bye, American Pie, drove the Chevy to the Levee, but the Levee was dry". Dry as in NO MORE FKIN BAILOUTS FOR THE RICH BSTARDS. This Namby Pamby way of thinking, that we can have it all and let someone else pay for it needs to end. Better now, than when we run out of oil.

C_A - You do not understand, THIS IS NOT A BAILOUT.

Yes the wealthy will make out like bandits as they always do but the issue is appeasing the creaditors of the Worlds largest Subprime Borrower, The USA.

If USA looses the ability to borrow then YES the World Will Suffer.

Cheer...... ah screw it.

I think everyone should let others know the problem and write to your local congressperson. They have e-mails. Tell them to vote no on ALL bailout packages or you will vote for whoever runs against them the next time they are up for re-election. They may actually listen to losing their jobs over this.

hey hey tirwin,

I did write my reps, and we do have some leverage over them, but not enough to stop the bill. They are caught in a catch-22.

a) If they vote no and the bill fails, they will be blamed for the economic fallout and it will hurt them at the polls.

b) If they vote yes and the bailout passes but fails to avert catastrophe then they will be blamed at the polls.

There are only two good solutions for getting reelected.

1) Vote with the minority so that the blame falls elsewhere.

2) Vote yes and pray that it works.

Since less than half can be in the minority the majority will vote yes and pray to the free markets or manifest destiny or whatever it is that they really believe in deep down inside, underneath all the spin and PR.

"I am so upset. The Simpsons and their fellow humans voted for your party instead of mine. Obviously they're catching on to the truth."

Um,yeah, well, I did. And all three of my congresscriminals have voted for the bailout. I went a step further and updated my blog with info then e-mailed around 25 family and friends about this issue. Looking at my stats from StatCounter, all but 2 or 3 visits have come via The Oil Drum, so... my efforts are failing miserably.

Sometimes I get a big insight or a lot of info from a seemingly innocuous source. This is one of those times. I reached out to 25 people... and nothing. (I don't even know if the few visits not directly via TOD were any of the people I e-mailed.) This is the US in a nutshell.

The party's over.

Cheers

It is a mechanism, which when viewed through the previously ignored lenses of conservation of mass, thermodynamics, and system complexity, has contributed to increased poverty, resource depletion, climate change, overpopulation, wage slavery, isolation, increased prevalence of disease, and a deterioration in mental health.

It is a fundamentally fairy-tale-based mechanism, because it durably ignores the problems it foments, and refuses to change in the face of mounting contrary experience.

Who is proud to defend Santa Claus or the Easter Bunny? Children.

The Financial Times needs to grow up.

"It is a mechanism, which when viewed through the previously ignored lenses of conservation of mass, thermodynamics, and system complexity,.."

What kind of BS gibberish is that? If I am trying to understand an economic problem I think I look to Friedrich Hayek or Milton Friedman, not Robert Boyle or Lord Kelvin.

"has contributed to increased poverty, resource depletion, climate change, overpopulation, wage slavery, isolation, increased prevalence of disease, and a deterioration in mental health."

Hello? Don't let facts get in your way here. Until recently what kind of governments did China and India have? What kind of government does Indonesia have? Have you checked their populations? Where democracy and capitalism flourish living standards go up and populations decline or go down. What has lifted the greatest percent of people out of poverty in South America? The answer is capitalism & Chile, now the wealthiest country in South America. I suppose you view scientific socialism in the former Soviet Union, Mao's China, Castro's Cuba, and Vietnam as successful? Yeah, that is why all but Cuba have abandoned socialism for capitalism. See India also.

Wage slavery? Try Cuba, everybody makes the same wage from doctors to street sweepers which is not enough to buy the minimum amount of food to exists on. Socialism gives you shortages of sugar and rationing in Cuba and Venezuela, countries that export sugar.

Last time I checked there was a finite supply of petroleum, coal, iron ore, tin, copper, and every other mineral; it doesn't much matter what your politics are.

You might be right about disease, and a deterioration in mental health; as something certainly has affected your ability to discern fact from fantasy.

Hayek and Friedman were flying to London form New York, and after toasting their successful policy to cut health care for the benefit of the unwashed masses to develop character, the pilot came on and announced that the plane had lost one of it's engines, but not to worry, as they have 2 and the flight will just take a bit longer. Friedcman turns to Hayek and says "I hope we don't lose the other, or we will never get down"

I think this is the point of superstition based economic models supported by the Hayek's and Friedmans of the world.

I agree that Friedman is an ass, but Hayek gets a bad rap.

If you read "Road To Serfdom", Hayek carefully describes the areas which free markets will be unable to address including, but not limited to, roads, hospitals and care of the elderly. He advocates that these needed services be provided by governments using tax dollars.

Free-market fundamentalist have absconded with Adam Smith and Friedrich Hayek; they put words in their respective mouths, and count on our having not read them. I believe, based on my reading, that Smith(and Hayek) would be appalled by what we justify in his name.

Yeah, as if:

1. Economics does not involve physical materials in the real world, governed by conservation of mass.

2. The recombination and exchange of physical materials doesn't involve energy and thermodynamics.

3. The societal exchange process does not involve systemic aspects of complexity and chaos.

4. Money is a real substitute for any of this.

5. That someone else's suckier-existence makes our suck not suck. That simply because it's worse in Cuba means it's not bad here, or everywhere for that matter.

6. That humans exist independently of the climate that's changing, or the species becoming extinct.

Your idea of economics is centuries old and is being proven wrong on the world stage as we speak. Almost as if it's just another religious fanatic talking.

But I do know where you're coming from, because I was educated to think in the same bullshit way you currently do, and it's totally wrong. And it took years of de-programming to get out of that limited, linear, wasteful way of thinking.

I wish you the best of luck in digging out the bullshit you have in your head. You could begin with "Chaos: Making A New Science", by James Gleick, "The Tipping Point", by Malcolm Gladwell, and "The Black Swan", by Nassim Taleb.

This is close to a thousand pages of material, which you will balk at because of a quick-fix mentality, for which I will recommend "Mastery", by George Leonard, in which he discusses the problems of addressing problems with quick, symptom-based, back-end solutions, as opposed to durable, cause-related, systemic approaches which take longer.

All of these are available at Amazon, P2P filesharing, and probably your local library.

To put it super simple: Financiers and traders groan or laugh and do high fives, “the market shows”, analysts say “the market tells us”, “the market decided”, etc. as if it were God or some superior entity to be obeyed.

Crucial decisions are given over to the collective, averaged accumulation, of a small class of people who ‘bet’.

The position is: the horse who wins is not the horse who wins the race, but the horse who most of the bettors expected to win the race! So you can do away with the horses entirely.

Now, that would be OK if the bettors just stayed amongst themselves, then they would soon see that things average out and their bets aren’t in the long run winning ones.

But these bettors drag in some huge % of ppl in the world who invest their money on the touted favorable odds... and can thru their actions manipulate the odds enough so that profits do come in for some time...

Votes are now at -12. Is there some way to see how many votes have been cast?

At first I was surprised by the leftist domination in the comments, but perhaps I should have sensed it when I got bashed for proposing nuclear power as a solution to our energy problems some time ago.

Why is it that those who worry the most seems to refuse rational solutions?

I am unaware of a way to see total votes but will ask SuperG.

I am pronuclear because I think we need everything we can get, but also pro- addressing end goals before we waste another 10 years of energy.

As to rational solutions, it is pretty evident that in times of crises (and even not), we are not exactly rational creatures, and will grab at anything that puts out the immediate fire. Thats why TOD exists, to try and get knowledge and awareness of the manifold issues that confront an energy constrained planet out in the open and discussed. Social equity - as measured by the GINI coefficient and in other ways - is one aspect of this problem - capitalism will be mightily stretched if 1% of the people hold 99% of the wealth. This is not a 'socialist' site, nor it is a 'capitalist' site - but I think in general, the contributors and commenters here recognize the current model isn't exactly working well...

Thanks Nate. About capitalism - I think wealth distribution isn't very interesting. For capitalists to hold 90% of all wealth is probably better for all than for the government to do it - it is merely a question of how to organize production. Of course we'll be screwed if super-capitalist consumes 90% of all income/production. Thankfully, they do not.

About the model not working well, I think capitalism and markets absolutely does their job. The system churns out products that are in demand in as high quantities that is humanly possible. And if you want to alter production or consumption patterns, all you have to do is regulate and pay the price of the resulting market disturbance.

So, since you can do whatever you want by voting in the right politicians, you aren't really dissatisfied with the system, but with the US voters, right? B/c if you all want to be like my country, Sweden, with $9/gallon of gas due to taxes, a car park with twice your MPG, low GINI and so on, you just have to decide to do this. (There is a price to pay, of course - a price that is bigger than you might think.)

Some of you seem to think that your political system is somehow rigged to make change impossible, but as an outside observer I think that view is partly conspiracy theory, partly contempt for your fellow voters. You can do whatever you like, actually, and I think your political life have a lot more energy and diversity than ours. You are definitely not more restricted than we are, just different.

1)I'm jealous - Sweden has a great deal of things going for it - very low population density (about 1/30 of California), high natural capital, low GINI, etc. Could you please enlighten us (because I have no idea), how you transformed your social system into $9 gas and 80-90% highest tax bracket? Was it in baby steps or all at once?

2)when I say the system isn't working well, I mean the human satisfaction or whatever pyschic measure of well being you prefer, is not improved by the 'churning out of stuff' as you say. Combined with finite resources, and our neural penchant for novelty and competition, this is a fast recipe for overshoot of all materials that matter, including the global commons, irrespective of the political system, as long as it is based on growth. I encourage you to read On the Origins of Energy Addiction (it's long but I (humbly) think worth it). Also check out www.thestoryofstuff.com

3)I don't believe in conspiracies either, but to believe that we could elect a truth-wielding, limits-to-growth-understanding, systems-thinking, EROI-calculating, wide-boundary-thinking, lower GINI espousing, future-generation caring politician in this country, let alone a whole faction of them, goes counter to 'the Peoples' voting interests. Their penchant for immediate gratification (a human one especially prevalent in 21st century USA), would be too strong to allow but a handful of votes for a politician talking about these things. I can't speak for Sweden, but in US, such a person running for public office would be far more likely shot than elected.

Hey hey Nate,

There is a simple answer to why Europe and the USA developed different approaches. The frontier, the existence of open space allowed the industrial revolution to progress along a different course in the new world. There is a good book about whether the UK should go the American or European route which delineates the split "the World We're In" by Will Hutton.

Europe allocated all the land a long time before the industrial revolution, so when real problems began to develop they were forced to renegotiate the social contract. The renegotiation was unpleasant though, things like the guillotine exemplify the period. In the new contract individual rights to wealth and property were tempered by the needs of social cohesion. The German constitution, for example, explicitly states that ownership of property incurs a reciprocal responsibility to the community.

In contrast the Americas was completely unoccupied. (ignoring, as we did, the native population) So when the situation became unbearable there was a safety valve, the frontier. If life became too oppressive one could always move west to stake out a claim and materially improve one's lot. This enshrined the primacy of private property in the American mind. The open spaces, wealth of natural resources, and primacy of private property are largely responsible for the suburbs and automobile culture today.

Our revolution wasn't against the wealthy landed elite it was against foreign control, taxation without representation was the phrase at the time. We did manage a limited political restructuring under the New Deal but it was just a quick fix, not a real restructuring. Since it was a political arrangement, not a revolution, those who lost out in the shuffle have resented it ever since.

Should this panic turn into the second great depression, as I think it will, we will witness a fundamental rearrangement of the American system and character. Assuming the country survives it will become a more perfect union, but the process is going to be really ugly.

Just a note about conspiracies. In the English lexicon the word has two meanings. Conspiracy with a capital C refers to cloak and dagger secret societies like the Masons,Illuminati and the military industrial complex. conspiracy with a lower case c refers to things like Enron, WorldCom, Aurthur Anderson, the Bush energy plan, and the military industrial complex. To conspire means to make decisions that effect others without their input or consent which may not be in their best interest. The lower case c variety happens all the time but it is commonly referred to as corruption. The question is where do you draw the line? Most people accept that politicians repay favors for their financial backers and that corporations do things that they shouldn't. Fewer people are willing to accept that the Iraq war was for oil. Fewer still believe that 911 was a false flag event. And only the tinfoil hats believe that some shadow group is trying to destroy the country for whatever reason. The question then is where is it reasonable to draw the line and, more to the point, how do you know what reasonable even means in a world you have no access to?

Yeah well since the tinfoil hat group has been more correct in their prediction than any other group, I'll throw my tinfoil hat in with theirs.

20% unable to find the US on a globe.

50% unable to find "the Iraq" on a globe.

4 million in prison.

Interest on the national debt exceeds $5000 per year for every household above the median income.

Eradication of Habeas Corpus, Posse Comitatus, and most of the Bill of Rights.

Hundreds of tazer deaths, and courts ruling that tazer death is just a sudden death syndrome.

Dozens of FEMA camps, with inward facing barbed wire and turnstyles being built next to railroad tracks. And various sites where tens of thousands of plastic coffins are neatly stacked. On youtube for all to see.

Microwave weapons and sound weapons available and ready to use against the population.

The list just goes on and on. All tinfoil hat stuff.

Nate, some attempts to answer:

1) Well, we don't have 80-90% tax brackets anymore - that was in the eighties. The highest nowadays are around 70%. Actually, we have quite high economic freedom overall, although still very high taxes and rigid labor codes. We are slowly getting even more free, actually.

The taxes on gas and income were done in baby steps, and much of the income tax is hidden, i.e. isn't regarded as a part of your salary. Actually, it is called "employer fee" - a type of newspeak designed to hide the true tax burden. Employers pay 32% of employee salaries (no cap) for social insurance programs.

That may be something for the U.S: Maximize taxes but try to hide them - and make services and social programs as broad and visible as possible. The goal is to try to make as many as possible think they really need the benefits provided. Free schooling, free health care, $100 per kid each month, 80% income insurance in case of health problems or unemployment and so on. Do all that and make the taxes seem low.

2) Happiness research is a new field, and I disagree with some of your statements based on what I have read. I'll try to read your links though.

3) As I said, you are dissatisfied with your fellow voters - not with the capitalist system in itself. But I think you have a political system than you might realize, and that the problems you state will be overcome in time.

The project head was explaining how they designed in special control features into the system to intelligently block out bad things from happening (ala Murphy's Law).

Of course, being a "free markets" guy myself, I laughed quietly to myself at how stupid all those engineers were. Don't they know that the "invisible hand" always comes in to do the right thing? It is a total waste of human intelligence to even bother with engineering, social or otherwise. (/sarcasm)

I'm an engineer too, actually. The systems we build does as instructed - all fault handling need to be explicit as the systems can't really reprogram themselves to cope with unexpected faults. The AIs aren't that far along, unfortunately.

Markets are more like nature itself - they contain sentient beings that are able to learn from mistakes, adapt, reorganize and survive in response to the unexpected. Also, products and companies are subject to the consumers' evolutionary pressure and thus has to adapt or close shop.

Governments can make regulations - to prevent mistakes already made and learnt from. Bear Stearns chairman lost a billion - no one in finance will want to repeat his experience. So the regulations will solve nothing, but will cost us in terms of bureaucracy and inflexibility - and perhaps they will even contain seeds for other crises.

Btw, during 1945-1982, the US were in recession 21% of the time. Then Reagan started to deregulate, and since then the US has been in recession 5% of the time. Volatility has clearly decreased with deregulation and globalization, without any adverse impact on average growth.

It's not even leftist per se, as much as it is pure willful ignorance. I looked at that post with the -29 rating, and said "whoa he must have insulted someone's mama". But no, nothing like that. It is amazing to know that the majority of the readers here do not understand the basic principles of the free market.

Nor do they understand that countries and economies are not governed by any economic model; they are governed by Hegelian principles. Mafia rule.

No matter what economic model you follow, if corrupt criminals control it and dumbed down morons vote for it through Hegelian manipulation, then bad things are going to happen. I bet every single person who rated down that post has no understanding of the damage being done right now by the SEC's selective ban on shortselling. I bet they all love it. And they're gonna love being in a bread line too. The disconnect is staggering, even on a site such as this.

1)I full well know the damage being done right now on the short-selling ban. If after it expires on Oct 17 they keep the public disclosure clause for large funds posting to EDGAR, short selling as we know it (and therefore liquidity, confidence and market function as we know it) will be over.

2)what is Hegelian manipulation?

pukeon,

Others can try to cope with what passes for analysis in your rant. I just want to note your ignorance of fact.

The reality is that Cuban doctors earn salaries many times higher than the salary of streetcleaners, they live in nicer houses than the average Cuban, and they travel. I met a very interesting Cuban medical doctor not long ago in Vancouver, B.C., who was there visiting his daughter, a student studying at a local university.

It appears you know even less about India and Indonesia.

Thanks for that perspective Toil...nice rebuttal.

Yeah, like a central driven economy includes the laws of thermodynamics and all that...

Free markets is only the respect for freely agreed contracts, respect for private property and individual responsibility.

Socialist interventions (by the almighty State) like the end of the gold standard, the creation of central banks, created the conditions to undermine free markets and to live in the actual economic La-La-Land, credit expansion without previous savings to support it, massive injections of junk money made out of thin air and all that economic voodoo.

Austrian economics explains it quite well.

A sound money policy, government as an impartial referee, respect for the individual (corporations are not individuals), would put capitalism and free markets under the domain of the public, as it always should have been, and not as an instrument of government corruption for the benefit of a few corporations, notably the financial/military/industrial complex.

A sound money policy would restrain credit expansion without previous savings, adding an incentive to well thought investments, penalizing bad investments and allocating more effectively the scarce resources. It would teach us to live with our means, respect the Natural capital and it´s limits, unlike the recurrent bubbles and the raping of earth promoted by an expansionary money policy.

I wonder why the first greens were called conservationists?!?

The major flaw in this type of free-market model is the belief that markets are 'self-regulating' when they obviously are not.

Free markets are self regulating. If we had free markets in the US you might observe that, but what you are observing are rigged markets, and of course they are not self regulating. Laws were passed to impose the will of government on markets in order to benefit few at the expense of many, and what you are witnessing is what happens when free markets are not allowed to operate, and socialism is substituted instead.

So if you don't like what is happening, please place the blame where the blame is due, and not on freedom.

The rigging of the market is frequently done by players in the market, viz Enron, and countless other cartels, price fixing, unfair competition and monopolies. It actually takes serious external regulation to ensure markets stay fair.

First of all monopolies are created by law. Very few companies have ever achieved "monopoly" status through competition, and those cases have benefit the markets because the player maintaining a dominant market position through competition must continue to please the market, unlike monopolies created by government who do not need to please anyone but themselves.

Cartels, price fixers, unfair competitors, etc, violate the existing laws and don't need regulation, but do need criminal prosecution. (We have laws against murder, so should you be constantly regulated and watched by government regulators to make sure you don't plan a murder?) Regulation just institutionalizes the fraud because it transfers management to regulators who become involved with the offending corporations, setting standards that allow misdeeds and at the same time precludes redress in court by those offended. It is foolish to just keep demanding more of what does not work in response to a failure of what does not work, and that is what demands for regulation and more regulation are. What we need is no regulation other than allowing free markets to work; we have had plenty of government regulation and very little free market regulation because there has been not much free market.

And again, I point out that this problem had its origin in the manipulative imposition of the debt based monetary system upon us by collusion between government and banking interests. This system involves creation of new money by electronic bookkeeping entry and printing press and then loaning of this money to the public and government at interest. If you want to talk about fraud, this is the biggest ever. This system displaced the free market gold/silver money system; even gold was made illegal to own by Roosevelt to prevent the free market monetary system. Because money could be expanded it was, and we went from m2 of $32.2 billion in 1933 to $7,712.9 billion now, an increase of 239.5 times, and the great majority was loaned into existence (a little came into existence to build bank buildings, which if you look around town are some of the nicest buildings around).

Anyone who wonders why we are facing a debt collapse just doesn't understand the monetary system. Particularly on this site, with the prior discussions of unsustainable compounding growth systems should immediately grasp why such a compounding money system eventually collapses. All the regulation in the world cannot prevent such a collapse. And as a matter of fact one of the major interventions into the operations of Fannie came under the Clinton administration which imposed upon them the necessity of making loans to those who could not otherwise afford them, hence the origin of subprime mortgages.

The "Anyone" line is an ad hominen attack rather than a reasoned discussion.

Many of us "are" aware that in the days of the dinosaur there was no money and therefore all of it has been made up out of thin air by use of printing presses, electronic book keeping, etc.

The bank is the government. Don't you yet get it?

Well I suppose my anger at a predatory system bubbles up upon occasion, and I probably should have expressed that part more politely. Thank you for reminding me that one catches more flies with honey than vinegar. However, there was plenty of reasoned argument which you did not address.

I think I quite clearly expressed my understanding that the banks and the government colluded to impose a predatory system on us, and that system is collapsing because it is unstable.

Gold and silver were not made up out of thin air as money, but were mined, and both have had a long histories as stable money, so your comment about dinosaur days has validity only to a fiat or debt based monetary system.

Are you really defending the Fed and fractional banking? And what are you hoping to achieve with your sarcasm? A slap upside the head?

Cheers

"Cartels, price fixers, unfair competitors, etc, violate the existing laws and don't need regulation"

These laws, inter alia, ARE the market regulation - which I said are required to ensure fairness. QED.

You have disproved your own argument.

My take on those calling for regulation is that they have never been involved with how government regulation works. If you ever had any experience with regulators, you would know that this is an unworkable approach.

I am retired, but worked as a CPA and had much inside contact with businesses and related government regulators, including IRS agents, State Insurance Commissioners, State Public Service Commissioners and HUD administrators.

Here are some examples of how it worked which I personally observed or was told in confidence by the parties involved.

A large Florida based insurance company kept a very nice deep sea fishing boat, mainly for use by executives, but it was also used to take out an IRS agent who examined the companies books every several years, with never an adverse finding (I was aware of servers potential tax issues). The examiner from the state insurance commission also liked fishing and also never gave the company any trouble.

An insurance company in Louisiana periodically met with agents from the Insurance Commission's office over lunch or dinner and drinks paid for by the company, plus perks like Sugar Bowl tickets were common.

A regulated gas utility in Louisiana was the worst. A state auditor would announce a visit in advance and tell the company's financial executive what information he needed, which would be prepared in worksheet form by the company. The auditor would spend most of the morning meeting with company executives which consisted mostly of visiting and drinking coffee and eating sweet rolls. The auditor would then be taken to a long lunch with company executives. When he returned he could collect the worksheets prepared by the company to submit as his own work, say his good bye and drive off with a trunk full of his favorite expensive liquors placed in his unlocked car trunk by the company.

HUD regulates subsidized privately owned apartment houses for low income tenants. In order to get rent increases a several month procedure must be followed eventually resulting in HUD's approval or denial of the rent increase. Cost always increased faster than rents, and with the delays in approval of rent increases many of these projects went into default resulting in the government insured mortgage being paid by taxpayers, even in cases where the HUD representative was well intentioned. And heaven help the owner of a project who had an antagonistic HUD employee overseeing his property, because that made it almost a certainty that there would be insufficient rent income to pay operating expenses.

The idea that bureaucrats are your saviors does not correspond to the reality of human interactions.

Couldn't agree more re: the (in)effectiveness of government regulation - this is especially true in healthcare, where I've spent the last two years of my career absolutely dumbfounded at the mediocrity (which leads to poor outcomes) that is a direct function of government regulations. It's a dangerous leap, but I can't imagine government regulation influencing a better set of outcomes in another industry. Forced mediocrity leaves the door wide open for "power" players to both assert personal agendas, collude with other like-minded (and resourced) players, and exploit those trapped by regulation. So back to the premise of revolution, what gets us to a revolution faster: implementing the bailout at the chagrin of the voters, or killing the bailout (and any type of imposter) and watching the ramifications on Main Street?

No one is saying that government bureaucrats are free of corruption or the final solution to all our problems. Yes, someone has to check the checkers.

But think about this: your large Florida based insurance company has to constantly worry that next year the IRS may send a replacement agent who doesn't like fishing or sweet rolls very much. So they have to keep their misdeeds tempered down to some extent just in case. If there were no government oversight then it would be a free market free for all in terms of corruption and cheating.

Yeah, I have to deal with brainless government bureaucrats also. Therefore I know what you mean. However, the alternative world where there is zero oversight would be far worse.

I agree.

Consider the credit cycle.

Pretend that you are a small bank.

What is your winning strategy?

This winning strategy is the opposite of what a regulator would want to do.

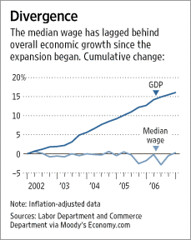

That's a pretty deceptive graph. By showing a divergence they imply that it shouldn't be that way (or that something is "wrong" because of it).

In reality, that exactly what you should expect such a graph to look like. The income figure is inflation adjusted and per capita... so you should expect it to stay essentially flat. GDP, on the other hand, should be expected to rise with a growing working-age population.

Change either GDP to "per worker GDP" or income to "total income" and the divergence is almost entirely erased.

Huh?

I'll grant the point that GDP also grows thanks to population increases, but that barely explains a couple percentage points in GDP growth over such a period.

But otherwise, you could not be more wrong. The fact is, until the 80s, GDP growth and BOTH per capita income and median wage growth were essentially identical. Since then, average wages have lagged somewhat, and median wages have lagged even more compared to GDP.

This reflects 2 things:

- a lower portion of GDP going into wages (corporate profits being a large gainer);

- increasing inequality within wage earners, as wage increases got concentrated in a small layer at the top, with most others getting nothing.

That graph is absolutely NOT what you'd expect - it's the reflection of massive transfers of wealth from the middle classes to a very small number of very rich people.

Then showing that data would be less deceptive.

And "corporate profits" go to people who risked their income to invest in the company... which is how it should be. So what's the problem? Look at the last year or so and wages have gone up while benefits from corporate profits (i.e. stock returns) have gone way down. That’s they “risk” that balances the “reward”.

What's your reference for that statement of fiction? Why should the profits of hard work go only to the investors who (may have) put up some of their savings to finance a venture, and none to the wage-earning workers who operate the venture, manufacture and assemble its product, sell it, ship it, track it, and collect payment for it?

Can you point out where I said "none" or "only"?

Why should profits go to the people who took the risk to earn them? How ridiculous a question is that? An employee and employer contract to have a certain job done for a certain amount of compensation (which certainly can include profit sharing if the employee is willing to risk that compensation if the company does poorly). The employee has the option of taking some of his/her money and investing it at risk if the opportunity for such gains is something desired.

Note that unlike the wage-earner, the owner not only has no assurance of income/profit... but can lose some or all of the investment.

Unlike the stock speculator, the wage-earner risks the main years of their life to actually make the company work, on the assumption that they can then retire with the contracted pension. Then when the wonderboyz speculate with borrowed money (if any) and destroy the company, the wage-earner loses both the job and the pension. Would the worker accept such terms, if discussed in advance? Perhaps, if there is no other (legal) way available to make a living, which is the situation arranged for him/her on purpose by those who are out to exploit.

One of the ways that is "arranged" is via the enforcement of a monopoly on the creation of "money". That worker cannot start their own business without financing. Perhaps they should simply "print" money, loan it out, and demand interest on the loan. Illegal, right? How come it's legal for "bankers"? The free market ain't.

The wage earner most certainly is not risking something to "make the company work". If the company fails he loses his ongoing income until he finds something else. The capital investor loses the investment. In some cases... everything they have.

And what decade are you living in? Pension? If he has one it isn't much at "risk" (with government backing), but few have one.

You don't think it's implied that if the company you elect to work for goes under, you could lose your job?

Oh please. The poor slave laborer. Why do you have such a low opinion of him? That's the only thing he's qualified to do?

Yeah... that's it... the problem is that people can't reap the benefits of property rights without having property? What a shock!

Of course they can start a business without financing... if they have their own capital. Just like the guy who started the company they work for did.

Had the Wall Street Boyz gambled with their own money, we wouldn't be in the fix we are in. It's all about "leverage", i.e., gambling with other people's money. That's not investment.

This is absolute insanity. The worker risks nothing?

1.Worker works for the company for X number of years at the opportunity cost of working elsewhere. The worker risks not working for a company that will grow, minimum.

2. The worker risks whatever physical/emotional ailments that might arise from the work.

3.The worker risks their time, i.e., their life energy. Also with opportunity cost.

4. The worker risks the company failing, thus losing a job, possibly pensions, stock options, etc.

5. The worker risks being laid off or fired at any time, and possibly at a time when other employment may not be possible due to age, etc.

Etc.

You say some really bizarre things, but this is beyond the pale.

I suppose you are right in theory but in practice I think not. Will bankers be losing money? Will their previous CEO´s be giving back their bonuses from last Christmas?

in the Anglo American model quite often profits don't go to shareholders, but are kept by management for their pet uses, ie takeovers, bonus payments etc. The weakness of the Anglo system is that it separates ownership and control. Managers can be reckless because it isn't their money at stake.

But who hired the managers?

Who knows? But for sure, not the shareholders.

Really? What're these "proxy" thingies I get every year for?

Am I not responsible for the actions of the people I vote for (including who they first and what actions they approve)?

Maybe your proxie thingies are different from mine. I get to vote from a pre-selected (not by the rank and file shareowners, either) list of Board Members. Not the management.

1) Shareholders have the ability to submit their own candidates.

2) The board is the management of the company in many ways.

3) The board selects the people you do consider to be managemnet.

The employees of a company have a more concentrated investment in their place of work than do investors of only money. There are only so many hours in a week that a worker can invest his time. Someone with especially good health and invests no time in his children, other family members, and the rest of the community may be able to split his time between 2 or 3 jobs while money investors can spread their risk among hundreds or even thousands of enterprises. If someone at the top of the company makes a stupid mistake hundreds and even thousands of employees, many of whom are excellent employees, may lose their income, pensions, health care, the chance of their children having a better life, etc. So who takes the bigger chance? The one who invests time and skills in a single company or the investor who spreads his risk among many companies?

That's nonsense... but even if true, they are compensated for that investment (wait for it) on exactly the terms they accept. The owner has no such security.

That just distracts from the issue. There could be a single owner or thousands.

That's dramatically overstated (unless, again, you assume that the american worker is an idiot with zero actual value - I don't). They "lose" it only until they move to their next job. The owner loses everything he invested.

What "massive transfers of wealth"? If I don't give you an ice cream just like that, have I "transferred" wealth from you to me? In a free economy, transactions are freely agreed upon - including employment and compensation.

No doubt, that is true in a "free economy."

Where in the world does such a thing exist? Not where I live. Not even in my relatively exalted position -- the Government and the insurance companies tell me what they will pay for my services, and I have no freedom to negotiate, nor can I collect more than their imposed payment schedule from patients -- by the terms of their unilaterally imposed contract.

I am free, of course, to refuse to participate with these entities, but the "free market" has seen to it that virtually no one outside their domains has any money -- the "uninsured" are unable to afford "insurance", or much of anything else.

Although insurance companies are free to combine against me to impose these contracts, if a dozen physicians get together to impose some sort of solidarity on the "negotiations" each contract year, then the Federal FTC will see to it that the upstarts are threatened with fines and jail time.

Medicine, like "Defense", and now we see "Banking" is nothing but corporate socialism.

I would be happy to compete in a "free" market. I have never seen one.

This _is_ what a free market looks like- when some players are bigger than the others. and why would you ever think the players would all be equals?

Technology is the very definition of inequality! the whole purpose of technology is to concentrate power. After many centuries with more and more advanced technology, power has been concentrated immensely. Individual people are no longer first class players in the free market. The biggest of the corporations, governments, and other large power structures, are the first class players. Set against them, an individual has no chance at all to compete. This is a free market, it's just that the nice little economics textbook stories about the farmer, the baker, and the village shoe maker, are hopelessly obsolete. In most of the industrial west, we have been able to preserve the _illusion_ of the textbook free market, but it's been just an illusion for most of us for a long time.

The decline in net energy available for civilization, though, will be accompanied by the unravelling of these immense power structures (though they will go down kicking and screaming), and an increasingly level field for competition - at a much lower level of scale and technology..

"Change either GDP to "per worker GDP" or income to "total income" and the divergence is almost entirely erased."

So go ahead and graph it - shouldn't be very hard. However, having looked at the data myself for per capita gdp (http://indexmundi.com/g/g.aspx?c=us&v=67) and median income (http://www.census.gov/hhes/www/income/histinc/p07AR.html) I can see your assertion is wrong. Per capita PPP grew 31.8% while median income grew 23.7% over that time period. I used the "current dollars" from the median income chart, but I'm not sure why it's so different from the 2007 dollars column. If the "current dollars" chart is nominal income, then we should be looking at the other column, which shows median income grew 2.7% in the time period being considered (2000-2007). I am not enough of an economist to know which column should be looked at. But, there are the numbers, check out the validity of your assertion for yourself.

Your two statements contradict each other. You claim that the data shows that I'm wrong and then post data showing that the original graph (showing a sharp increase in GDP with no increase at all in incomes) was deceptive.

Take into account that the two use different measures for "inflation" adjustment and the gap is even smaller.

In a capitalist nation, you can't expect the gap to be nonexistent.

I quoted the part of your statement I was taking issue with. 31.8% and 23.7% is not virtually eliminated in my opinion.

"Take into account that the two use different measures for "inflation" adjustment and the gap is even smaller."

I think you have it backwards. Take the difference into account and the gap probably becomes much bigger. But you don't seem keen on backing up your assertions with much argument or data.

Compared to 16% vs zero?

So you believe that CPI is a smaller figure than the inflation adjustment to GDP?

I am doing your research for you again. See this page: http://www.census.gov/hhes/www/income/histinc/constdol.html

It explains that "current dollars" means not adjusted for inflation. So, scratch that 23.7% rise in median income. As I suspected, the adjusted rise in median income for 2000-2007 was the 2.7% number I mentioned that you ignored.

PPP GDP takes into account both inflation and currency valuation changes. Obviously, the US dollar has suffered quite a bit in the past 8 years in international value, which makes the 32.8% rise in our PPP GDP pretty dramatic (because it rose that much despite considerable currency devaluation). So, median incomes rose 2.7% and GDP PPP rose 32.8%.

So yeah, 32.8% compared to 2.7% still seems to be a bit of a gap ;-)

You clearly confuse Capitalist with Corporatist / Fascist.

The US population grew by 6% between 2000 and 2006 whereas GDP as grown by 15%. Corrected for population growth, the GDP per capita would have grown around 8%.

Ok so the "free market" has its problems, but what is the alternative?

The free market may in realitiy be inefficient, but it is more efficient than the alternatives that have been tried over the years. And remember that the modern form of a free market grew out of the peasants revolt in the UK (among other things) in the 1300's after the first Great Plague, as the depopulation gave power to the peasants then working the fields.

The issue is that problems like we are seeing today will always result from a free market, which is why we are supposed to have regulations and regulators, to try to make sure things are pushed in the right direction, and there are floors and caps to prevent excesses, in particular the issue that free markets will allways tend toward a short-termist approach to everything.

The current crisis grown out of a failure of regulation, not the free market mechanisms that caused it (they worked fine, creating new ways of making something more efficient, ie the lending of money).

I suppose it depends how you define "free markets"? How would you describe the US economy in the 30 years after WW2?

I agree with your point about regulation - regulation is needed for free markets to function properly. But we're living in times where any mention of regulation gets you insulted, and all our politicians and pundits see no solution other than yet more deregulation.

The free market has one HUGE problem. It does not exist.

The problems unregulated free market creates have been known and well understood since the Great Depression. This makes it how long... 80 years?

Question: how do we always end up with the same type of crisises, even though we know very well the reasons for them?

Answer: the free market itself naturally creates enormous concentrations of wealth in just a few hands. Over time this economical power turns into political power. Using their obtained political power, those centers of wealth resists any regulation and any measures to protect the long-term public interests.

In short the whole system becomes corrupt. By its nature the so-called free market corrupts the politico-economical system. Therefore it is imperative that the market and private enterprises are a secondary system in a society, remaining under direct public check and observation every step of the way. Any system that loses the primacy of of the public interest is headed for a disaster in the long run.

You may not realize it, but you essentially recommend institutionalized corruption as a cure for ad hoc corruption.

I recommended nothing. Corruption is being fought with laws and institutions to enforce those laws.

There are countries with strong institutions and laws and others where those institutions are being bought and paid for by private interests. It seems to me in US we are having the whole government being bought by the Wall Street gang. Hell our financial minister used to be a chairman of the biggest bank... How is this possible at all?? I think all this was set up long time ago - I would date it at the moment the FED (a collection of private enterprises itself) was established and started persuing its "dual" goals of "growth" vs stability. The purpose of a central bank should be the stability of the financial system! It is not to sponsor some corrupt gamblers or save their asses when they fail on the expense of all of us.

It's not rocket surgery. This has all been clearly sorted out long ago by trial and error. Ask Eisenhower, Roosevelt. EVERY well-functioning market economy needs STONG government oversight and regulation to function properly. Note Canadian economy, where banks were never allowed by regulators to invest beyond the same fixed multiple of their assets and that multiple hasn't changed in decades. Govt. mortgage insurance was and still is restricted to only those mortgages where the buyer puts up a 10% down payment. House values are restricted to what an independent appraiser says, and the appraisers have no incentive to inflate.

Only one Canadian bank, CIBC, had any significant losses in the stupid "Sub-prime" fiasco, $300 million (not a serious problem for them). Serves them right for dipping into the US mortgage market which was OBVIOUSLY out of whack for years.

Also noteworthy, Cdn governments all are running surplus, have been for years, voters demand it. $9.2 billion federal this year. And big automakers say they prefer to locate here because universal medicare takes a huge direct and administrative cost off their books. And BTW, in Canadian medicare, doctors and hospitals etc. are still independent private businesses. Just that they send heir invoices to the provincial gevernments not HMO's. And there's no 25% of medical costs spent on insurer administration either.

THAT's what a free MARKET economy is supposed to look like, not that stupid neo-con nut-job you yanks are running.

And BTW, house prices are STILL gradually going up in most of Canada.

As a Canadian, I think you oversell us a little bit.

Govt. mortgage insurance was and still is restricted to only those mortgages where the buyer puts up a 10% down payment. This is actually not true. CMHC-backed, $0-down, 40-year mortgages have been available for a couple years now, but in response to the US housing crisis, they are being eliminated soon (off the top of my head, at the end of the year, but I could be wrong about the timing).

Only one Canadian bank, CIBC, had any significant losses in the stupid "Sub-prime" fiasco, $300 million (not a serious problem for them). Actually, there's at least $32 billion in asset-back paper that was bought in part by all of the major banks as well as some larger pension plans and other interests, which is currently locked up in a government-mediated plan to convert them, from what I hear, to long term bonds. This is separate from major writedowns that ALL major banks have made in the last year and a half, not just Scotia. But you're correct in that the amounts don't seem overwhelming, if nonetheless large.

Also noteworthy, Cdn governments all are running surplus, have been for years, voters demand it. $9.2 billion federal this year. And big automakers say they prefer to locate here because universal medicare takes a huge direct and administrative cost off their books. All fairly accurate. I'm not sure voter demand for continued surpluses is a dealbreaker, to be honest, but we don't really have a federal party currently strong enough on other grounds to get away with deficits (absent some pressing external justification, like, say, a serious recession...).

THAT's what a free MARKET economy is supposed to look like, not that stupid neo-con nut-job you yanks are running.

It's a mixed market or social market economy. I don't know how you can justify calling it a free market, and I don't know why you'd want to, either.

And BTW, house prices are STILL gradually going up in most of Canada.

Less and less gradually with each month. It's still difficult to say whether this is a levelling or the beginning of a downward slide or something more dramatic. The fact simply doesn't prove your point.

I have a book called "Saving Capitalism from the Capitalists", written by economists Raghuram G. Rajan & Luigi Zingales.

One thing they point out is essentially what you have just said: the incumbents in an industry can (& frequently do) "...capture the policy-making process and enact anti-market legislation" (p. 201). Furthermore, "the problem is particularly acute for mature firms. Because of their size & past successes, mature firms face limited competition. They also generate tremendous amounts of cash and, with limited legitimate investment prospects in their existing businesses, have no need for new financing," (p. 59). This means they often have very large sums of money to devote to capturing the political processes and further skewing the playing field in their favour.

Unfortunately, their prescription is to open up national borders to international competition, but this simply ignores the fact that all that does is expand the problem to the international level (i.e. you wind up with transnational industries with incumbents that have even larger sums of money to use for subverting the political process in even more regions).

By LevinK: "...the free market itself naturally creates enormous concentrations of wealth in just a few hands. Over time this economical power turns into political power."

I think it is the rigged market that concentrates wealth in just a few hands. The ultimate concentration of wealth was the southern plantation before the Civil War. Was this a free market in employment or a slave system? Without laws (government intervention in the free labor market) to support slavery and return run away slaves, the free market could have prevailed and slavery could not have been enforced.

Historically the most bell shaped distributions of wealth have occurred in periods characterized by freedom, and the most skewed distributions have occurred during periods of slavery (wealth for the few and poverty for the many). Free markets produce a normal distribution; rigged markets produce a skewed distribution. Transfer of wealth to the privileged group is the purpose of, or in some cases unintended consequence of interference in the free markets.

So instead of incorrectly blaming the free market, maybe it would be better to blame this screwing on government laws that rig markets.